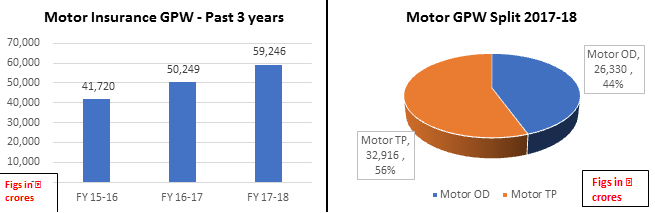

Motor Insurance is also called as Car (Two Wheeler) insurance, Vehicle insurance or Auto insurance. As the name suggests, a motor insurance is an insurance for two wheelers, cars, trucks, motorcycles, etc. The basic purpose of Motor insurance is to provide financial protection against physical damage to the vehicle or bodily injury to third party as a result of accidents, collisions apart from liabilities arising from such incidents. Motor insurance gives protection to the vehicle owner against (i). damages to his/her vehicle and (ii). pays for any Third Party Liability determined as per law against the owner of the vehicle. Third Party Insurance is a statutory and legal requirement and hence every vehicle owner should mandatorily insured his/her vehicle at least for Third Party cover. The owner of the vehicle is legally liable for any injury or damage to third party life or property caused by or arising out of the use of the vehicle in a public place. Driving a motor vehicle without insurance in a public place is a punishable offence in terms of the Motor Vehicles Act, 1988.

Motor Insurance is also called as Car (Two Wheeler) insurance, Vehicle insurance or Auto insurance. As the name suggests, a motor insurance is an insurance for two wheelers, cars, trucks, motorcycles, etc. The basic purpose of Motor insurance is to provide financial protection against physical damage to the vehicle or bodily injury to third party as a result of accidents, collisions apart from liabilities arising from such incidents. Motor insurance gives protection to the vehicle owner against (i). damages to his/her vehicle and (ii). pays for any Third Party Liability determined as per law against the owner of the vehicle. Third Party Insurance is a statutory and legal requirement and hence every vehicle owner should mandatorily insured his/her vehicle at least for Third Party cover. The owner of the vehicle is legally liable for any injury or damage to third party life or property caused by or arising out of the use of the vehicle in a public place. Driving a motor vehicle without insurance in a public place is a punishable offence in terms of the Motor Vehicles Act, 1988.

Request a Call Back

Thank you for contacting us