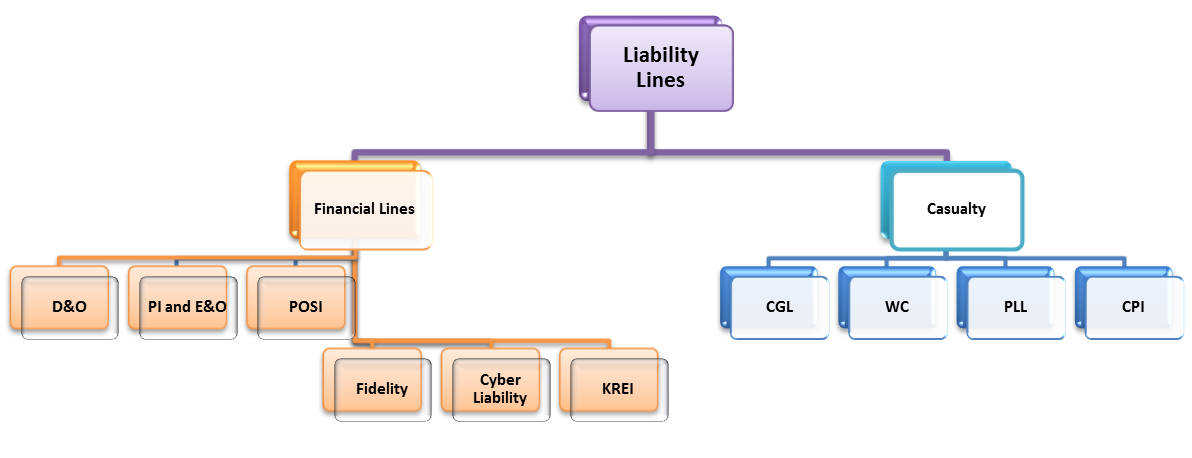

Public liability insurance or general liability insurance covers a business or organization against claims if its operations injure a member of the public or damage their property in some way. The common policies under Liability Lines are:

- Directors and officers liability insurance (D&O) -protects an organization from costs associated with litigation resulting from errors made by directors and officers for which they are liable.

- Professional Indemnity & Errors and Omissions Insurance (PI & E&O) -protects insured professionals such as architectural corporations and medical practitioners against potential negligence claims made by their patients/clients. Professional liability insurance may take on different names depending on the profession. For example, professional liability insurance in reference to the medical profession may be called medical malpractice insurance

- Public Liability Insurance -covers the cost of claims made by members of the public for incidents that occur in connection with your business activities. It covers the cost of compensation for personal injuries, loss of or damage to property & death. Policies vary from insurer to insurer, but most public liability policies cover for incidents that occur on insured’s business premises, or that take place off-site, at events or activities organized by insured’s company

- Cyber Liability -Cyber Insurance is an insurance product used to protect businesses and individual users from Internet-based risks, and more generally from risks relating to information technology infrastructure and activities. Coverage provided by cyber-insurance policies may include first-party coverage against losses such as data destruction, extortion, theft, hacking, and denial of service attacks; liability coverage indemnifying companies for losses to others caused, for example, by errors and omissions, failure to safeguard data, or defamation; and other benefits including regular security-audit, post-incident public relations and investigative expenses, and criminal reward funds.

- Commercial General Liability -Commercial General Liability is the specific name for a policy of this type in the United States insurance market. It is the "first line" of coverage that a business typically purchases, and covers many of the common risks that can happen to any type of business, such as bodily injury or property damage on the business premises or due to the business operations, personal and advertising injury, and medical payments.

- Environmental liability –Also called environmental impairment insurance protects the insured from bodily injury, property damage and cleanup costs as a result of the dispersal, release or escape of pollutants.

- Contaminated Product Insurance -Contaminated Products Insurance provides cover for recall costs, loss of gross profits and rehabilitation costs following either accidental or malicious contamination (whether actual or threatened). Adverse publicity and governmental recall are additional triggers which have recently been introduced and will be automatically included, subject to the geography the insurance product is provided for.

- Workmen Compensation (WC) -employers’ liability required by law if you have employees – covers the cost of compensating employees who are injured at or become ill through work. If you are an employer you are legally obliged to have employers’ liability insurance. Other types of liability insurance are optional.

- Product Liability -covers the cost of compensating anyone who is injured by a faulty product that your business designs, manufactures or supplies