Tips to find best travel insurance

Tips to find good and adequate international travel health insurance.

Know more »Travel insurance in Indiaprovides coverage for medical expenses incurred overseas for any treatment received as an inpatient or outpatient. All plans also cover trip related exigencies like trip delays, trip interruptions, trip cancellations and related problems that may arise during your trip. Some plans also provide services such as travel-related advice, Medically required Evacuation to your home in India or a hospital overseas for continued medical treatment. Other assistance services include providing emergency cash or help in the event of the loss or theft of your money, valuables or travel documents.

You have an option to compare differenttravel insurancepolicies online in E India Insurance and then choose the cheaper one according to your requirements. As an insured, please note that "cheap" may also mean limited insurance coverage. So kindly evaluate and decide the cover requirement based on your age, destination and duration of travel and then look for the most affordable option.

Buying travel insurance online is easy. All you need to do is, follow the instructions on our website, enter your personal details and buy using your credit card. The purchase is done on a secure page, and your credit card information is safe.

The insurance can be purchased from anywhere across the globe as long as the traveler is still in India. A son or daughter sitting in the United States or the United Kingdom can purchase insurance for their parents who are traveling from India.

All the relevant details about the policy is available online, so you can make an informed decision while purchasing the plan, and not depend on the decision of your travel agent or insurance agent.

Buying business insurance online saves time as it is convenient and can be completed in a matter of minutes without any paperwork. Purchasing online is environmentally friendly as there is no paperwork involved.

You can also use thecompare travel insurancetool, where you can compare travel insurance policies offered by several companies under one roof and buy the policy you like.

No, you do not pay anything additional. You pay only for the cost of the insurance policy. Our online facility provides the best prices; you cannot get a lower price for the same product anywhere else.

You can always save money by comparing quotes of different insurance policies. There are many insurance companies offering attractive policies, you can compare the different plans using ourIndian travel insurance comparisonfacility. Select the policy suitable to your budget and requirements. If you travel overseas regularly then the annual multi-trip policy probably works best.

You can purchase using either credit card, debit card or cheque on our website.

No, there is no such requirement to getting medical test fortravel insurance. Some companies might ask for medical tests for travellers more than seventy years for higher coverage. Coverage often to fifteen thousand dollars is provided without medical tests.

For most of the travel policies offered on our website, there is no need for providing medical records. If medical records are required then it’s clearly mentioned.

You will receive the policy document by email and a hard copy of the same document will also be sent to your Indian address by courier.

In case the courier is delayed, you can use print out the electronically sent soft copy which is a legal document and is fully valid.

In case the policy has not yet started then contact the company and request for the cancellation. If the policy has already started then you have to get in touch with the company and provide all the pages of the passport as proof that you have not travelled overseas. In both the cases the cancellation charges is Rs.250/- per policy.

The insurance policy will provide details for filing a claim. You should submit the claims form along with all other relevant documents (medical bills, doctor’s records ...) to the claims office. There will be a claims support telephone number who can assist you in this process.

TATA AIG, Bajaj Alianz, Reliance, ICICI Lombard, Oriental, Cholamandalam, Apollo DKV and Future Generali are some of the companies we work with.

Passport loss, baggage delay, baggage loss, accidental death while traveling, either during the journey or during the stay outside India is some of the emergencies according to insurance companies.

While it is not mandatory for you to carry the policy, we do recommend that you carry the document when travelling and refer to it whenever necessary.

All your premiums go into one big pot and are called as pooling of risk. The premiums collected are utilized to provide financial support of those travellers who need assistance.

Yes, you can visit any hospital. All insurers have assistance companies that provide coverage throughout the world. If time permits the insured is advised to contact the assistance company.

Yes, most of our policies include Baggage loss, Trip Cancellation, and Emergency Repatriation.

No, your return journey will not be covered under baggage delay benefit.

No, it does not cover rental car insurance when you are travelling.

Of course you can buy a policy. Please use our'Indian travel insurance comparison'to see plans that you can purchase.

Yes, as long as the treatment is an emergency and it is on natural teeth.

The 'Planned Hospitalization' is scheduled for a future date either for treatment or surgery based on doctor's advice. On the contrary the hospitalization that occurs in an unanticipated circumstance for example, due to accident or a medical emergency is called as `Emergency Hospitalisation'.

GenerallyTravel insurancewill not cover adventurous sports but there are specific policies which do. For more details contact us.

TPA stands for Third Party Administrator

No, the definition of family is that of a couple and two children. Nieces and nephews are not included within the family and are not covered within the family floater insurance policies

You have to call the toll free number on theTravel insurancepolicy document and the customer care executive will guide you.

Yes, most of our policies include Baggage loss, Trip Cancellation, and Emergency Repatriation.

No, your return journey will not be covered under baggage delay benefit.

The maximum duration that most insurance companies offer coverage for is 180 days under a single trip. However there are some insurance companies which offer an insurance policy beyond 180 days subject to an underwriting approval post a request from the insured. If the insured is traveling for a duration longer than 180 days, it is better to reach out to our customer support team, who will help you get a policy for covering the entire duration of your trip.

UK is not part of the Schengen Agreement and therefore a Schengen visa as such does not allow you to enter the UK. Some insurance companies offer a specific Schengen Insurance plan, which will not be valid for travel in UK and the insured must buy a separate policy for UK travel. However some insurance companies offer a Excluding Americas plan without sublimits and this plan is valid for travel through Schengen countries and UK. Please go through the terms and conditions prior to purchasing the ideal plan.

Some of the criteria include:

Travel insurance must be a priority when you’re travelling abroad, irrespective of whether you are travelling on business or leisure. Some business travellers could have an insurance coverage provided by their employer, and hence purchasing a separate plan may not be required. But these company business policies may not cover family members. It is important to note that the retail plans have a more comprehensive coverage, and hence it is recommended to purchase a separate policy even for your business travel.

Most insurance companies do not specifically provide the list of network hospitals across the world. It is recommended for the insured to call the Assistance Company (on the toll/toll free numbers provided on the policy certificate) who will direct them to the best available hospital facility depending on the nature of treatment to be availed. In case of an emergency the insured can be admitted to any hospital across the world, and the Assistance Company will ensured cashless coverage subject to admissibility of the claim.

Daily allowance is a reimbursement of all incidental expenses, upto the policy limit, that is payable to the insured during their period of hospitalisation (being an inpatient). The policy specifies a limit per day payable, and the deductible of 1 day is applicable.

If you have had the bypass surgery within 48 months prior to commencement of your travel/trip, then the same will be treated as a pre-existing condition under the policy and any claim/treatment occurring as a result of the surgery, will not be covered under the policy. Similarly if 48 months have elapsed since the surgery, but you are still under continuous medication for the bypass, the same will be treated as a pre-existing condition and excluded under the policy. Some insurance policies have a limited coverage for pre-existing conditions in life threatening conditions, this could provide some coverage subject to other terms and conditions of the policy.

If you are still under continuous medication for diabetes, the same will be treated as a pre-existing condition and excluded under the policy. Some insurance policies have a limited coverage for pre-existing conditions in life threatening conditions, this could provide some coverage subject to other terms and conditions of the policy, if the life threatening condition is a result of you being a diabetic.

Sublimits are extra limitations in an insurance policy's coverage of certain losses, primarily Sickness Medical expenses. They are part of the original limit, that is, they do not provide extra coverage, but set a maximum limit to cover a specific loss or for a specific medical expense. Sublimits can be expressed as a dollar amount or as a percentage of the coverage available. Typically they are part of the policy for insureds with advancing age.

For example, in a travel policy which has an Accident & Sickness Expense coverage of $100,000, it might have a sublimit of $10,000 to cover Surgery Expenses. This means that only $10,000 of the total coverage can go toward paying for Surgery Expenses. The insured cannot receive an insurance payout of an amount exceeding the sublimit for the types of loss specified.

You are free to visit to any doctor/medical practitioner/hospital, provided they are licensed by the local Medical Council and acting within the scope of his/her/their license. The practitioner should hold a degree of a recognized institution and be registered by the Authorized Medical Council of the respective country. It is however advisable to call the Assistance Company (on their toll/toll free number) and seek their direction regarding the same.

If the treatment, tests, medication are expenses that you have necessarily and actually incurred for medical treatment on account of Illness or Accident on the advice of a Medical Practitioner, the same would be covered under the policy. This is however subject to the fact that the expenses are incurred for a condition admissible under the policy.

Pregnancy and all related conditions, including services and supplies to the diagnosis or treatment of related conditions, including surgical procedures and devices are all excluded under the coverage of the policy.

The medical expenses incurred due to this accident will be covered under the policy, subject to you not being a professional sportsperson participating in a professional sport; or you participating in a professional sport for which you are untrained. It will also be covered subject to you not putting yourself in needless peril.

Travel Insurance provides you and your family medical, non medical and other assistance in case of an emergency while travelling on a Domestic or International Trip; irrespective of whether you are a business or leisure traveller. Insuring your trip ensures a stress free and enjoyable holiday.

No, there is no medical examination required upto the age of 70 years for most insurers. Some insurers ask for a few tests to be conducted post 70 years. If the insured declares having some medical history, the insurer could ask for medical reports to approve purchase of the insurance policy.

Most Insurance Travel Plans provide coverage to travel trips as short as 1- 4 days.

The key factors influencing the premium are the Age of the traveller, Destination of trip, Duration of travel and the Accident & Sickness Sum Insured opted for.

A ‘Pre-Existing Illness/Condition’ is one with which the person is already suffering from and is availing ongoing medical treatment when he/she buys the policy. It could also be related to a major surgery that the insured has had in the recent past. Some insurance plans do not cover pre-existing diseases, whereas a few others cover the condition in “Life Threatening situations”.

Foreign nationals in India who have a Work or Residence Permit and are based in India are eligible to buy an insurance policy from an Indian insurance provider.

The insured will need to submit an email request for extension and the extension policy can be purchased post approval from the underwriter/insurer.

Travel Insurance is not mandatory for Domestic Travel within India. While travelling abroad, only Schengen Countries have a mandatory requirement for insurance prior to granting a visa. However given the cost of medical treatment abroad, it is advisable to insure yourself every time you travel in India and abroad.

The Schengen countries with mandatory travel insurance requirements include Austria, France, Latvia, Norway, Sweden, Belgium, Germany, Lithuania, Poland, Switzerland, Czech Republic, Greece, Liechtenstein, Portugal, Denmark, Hungary, Luxembourg, Slovakia, Estonia, Iceland, Malta, Slovenia, Finland, Italy, Netherlands, Spain.

The policy can be cancelled via a written request sighting the reason for the cancellation. The policy can be cancelled anytime prior to the inception of the policy. If the policy has already incepted and the insured has not travelled for some reason, a copy of the complete passport needs to be submitted as a proof that the journey has not been undertaken. Cancellation charges of Rs. 300/- shall be applicable and the balance premium shall be refunded.

No refund is allowed for an early return to India under any circumstances.

Each insurance partner works with their respective Assistance Partners across India and abroad. While abroad for any assistance/claim, the insured should reach out to the Assistance Partner on the Toll/Toll Free number which is provided on the policy certificate. If however, you have returned to India, you can get in touch with the insurance company directly and register a claim.

On registration of a claim with the Assistance Partner or the Insurance company directly, the claim form will be forwarded to the insured. The forms are also available on the website of the respective insurance companies. The insured will need to submit the claim form with the supporting documents for processing the claim.

The Assistance/Insurance company will pay up to 100% of the claim (subject to the policy terms and conditions and upto the maximum Sum Insured availed) above the deductible amount (mentioned on the policy certificate) to the medical facility. This will be done either by placing a Guarantee of Payment (GOP) or making a payment to the hospital. This is subject to eligibility of the insured for coverage.

The deductible under the Accident & Sickness is normally USD $100 .The policy deductible is applicable for each instance of sickness/ailment. For continuous treatments relating to the same sickness, the deductible will only be applicable once. The insured is required to quote the Claim reference number when contacting the assistance company while undergoing follow up / re-revisit treatments. The deductible will need to be paid in each instance of a new/ different ailment / sickness.

During discharge of the patient and on preparation of the final bill, the deductible mentioned in the policy schedule is payable by the insured. Apart from this, all expenses that are not payable under the terms and conditions of the policy will also have to be paid by the insured to the hospital / medical facilities. The Assistance/Insurance company will directly pay the allowed expenses to the hospital.

It is advisable that the insured contacts the Assistance Company who will direct them to a Network Hospital in the same locality and assist with a Cashless facility. There is no restriction on the hospital where treatment should be taken. The treatment can be taken in any hospital However, the hospital should be a registered hospital under the local jurisdiction.

Yes, passport loss is covered in the policy. Compensation for expenses incurred directly in obtaining a duplicate or new passport abroad.

This benefit will reimburse the insured for the loss of checked in baggage in the custody of the common carrier as per the coverage available under the availed plan.

Compensation for reasonable expenses incurred for purchase of emergency personal effects like toiletries, clothing, medication etc. due to delay in arrival of checked in baggage, whilst overseas.

No, if later the baggage and/or personal belongings are lost, then any amount claimed and paid to an Insured Person under the baggage delay will be deducted from any payment under the Baggage Loss.

Accident & Sickness Medical Expenses includes ambulance service (to or from the Hospital).

In the event of medical emergency, the Assistance Partner will arrange for evacuation and transportation based on the evaluation of your medical condition. The Assistance Partner also provides for repatriation of remains in case of unfortunate death of the insured while overseas.

If the Common Carrier in which the insured Person is aboard is hijacked, the company agrees to pay to a Distress Allowance in excess of the Deductible.

The country where you propose to spend the maximum duration of time (during the entire trip) should be selected.

Care should be taken to ensure that the departure and return dates are in line with the air tickets purchased to ensure coverage during the entire trip. It is advisable to add 1 day before and after the air ticket dates to ensure the time differences between India and the country being visited are also taken into consideration.

The insured’s completed age in number of years should be captured while getting a quote. However please note that some insurers calculate the age of the traveller on the date of travel, and this could result in a revised premium while purchasing the policy, if the insured has his birthday between the date or purchase of the policy and the date of travel and this results in a change of the age band.

Please send us an email regarding the same and we will arrange for a duplicate copy to reach you prior to your travel. You will also receive a sms with the policy number, this is sufficient for any interactions with either the Assistance Partner or Insurance Company.

If you're going on a cruise and need cover, conditions will vary from insurer to insurer and some may not cover cruises at all, therefore it is essential that you read the policy documentation prior to taking out a policy. You will also need to check that all countries you are going to visit during the cruise are covered. When using our site to book this type of insurance, we recommend that you select the furthest geographical destination for your holiday and then check with the insurer they will cover all the other countries/destinations that are scheduled for your trip.

At present you will need to purchase your cover online by searching for the most appropriate policy for you. In order to help, we have provided some guides to help you choose the best policy, your choice will be single trip and annual multi-trip. A single trip policy will provide coverage for a specific holiday or a single trip. Simply select your holiday destination and then your holiday start date and end date. An annual multi-trip policy is a travel insurance policy valid for 12 months. The main advantage of an annual multi-trip policy is that you do not have to arrange cover for each journey that you take, especially if you and/or your family travel frequently throughout the year. It also generally works out better value than buying two or three single trip policies a year.

If you still need some more assistance, we will be glad to help you over a call.

A pre-existing condition usually means any medical condition for which medical advice, diagnosis, care or treatment was recommended or received. It is always a good idea to speak to the insurer you are thinking of using to check whether they will include your condition on the policy.

For example, If you're pregnant, certain exclusions may apply if you travel after a certain point during the period of your pregnancy. We would advise you to read the policy wording thoroughly, prior to purchasing the plan to see at what exclusions and other conditions may be in place.

We are happy to make changes/updates such as your address, title and surname (in event of marriage) on policies purchased on our site. We may also be able to change your travel dates as long as your trip duration remains the same and your trip has not yet commenced.

We will however not be able to make policy changes that will affect the premium of the policy. This includes increasing or decreasing the Sum Insureds (change in plans) or adding or deleting persons to any policy. If you wish for your policy to be changed, and your trip has not commenced, we will be able to cancel and reissue a policy with the revised details.

Your policy will expire at midnight on the final day it's valid for. For single trip polices your cover will end on the day you have advised you will return to India as per the policy certificate or on the date of your actual return, whichever is earlier. For an annual policy your cover will expire a full year later so, for example, if you purchase on the 2nd of February 2016, your policy will expire at midnight on the 1st of February 2017, by which time you must be back in India.

If you are having problems completing payment this may be for several reasons. The majority of issues are usually related to your card provider. We suggest that in the first instance you check to see if your card has had any issues; any issues around this can be answered by your bank. However, should you have a payment fail during your purchase process, please close your browser and wait before competing your search and purchase with an alternative card. We appreciate this may cause some inconvenience, but we do this to prevent any type of card fraud from taking place.

Details of cover can be found in your policy documentation regarding disasters and terrorism. Most insurance plans offer coverage for these eventualities, but there may be exclusions within your policy so it's important that you check this if you're concerned.

Medical costs abroad can be very expensive and without adequate insurance cover you could be left severely out of pocket.

Yes, once you have chosen the insurance provider on completing a few more personal details you will be directed that insurance provider where online payment can be made.

Yes, if you prefer to speak to someone about your insurance purchase, please call us at our Assistance number mentioned on this site and we will come back to you at the earliest.

Travel Insurance can take much of the worry out of a bad situation by paying for covered medical evacuation required to transport you to the nearest hospital with required medical facilites. In addition, assistance services are included to verify coverage so that you can be treated immediately. The assistance services can also help you communicate with the doctors if you don't speak the same language. Without the medical coverage included in a Travel Insurance plan, you may be forced to pay out of pocket up front for medical treatment and medical transportation, and you'll be on your own dealing with the doctors and the hospitals in a foreign country.

Firstly take a look at what insurance coverage you may require based on where you are traveling to, duration of travel. Then review all insurance companies and their plans…Take factors like Reputation of the Insurer, Assistance Partner abroad and their hospital networks across the world, Claims settlement capabilities. Thirdly, review the cancellation and refund policies applicable to your trip so that you know what the penalties are and when they will go into effect. This includes fees/penalties charged by all vendors including cruise lines, airlines, hotels, transfer companies, tour operators, etc. Contact the insurance provider directly if you have specific coverage questions.

A traveller must first realise that there are many insurance companies offering Travel Insurance plans in the India market today. They should also understand that in Travel Insurance, one size doesn’t fit all…this means that just buying a Travel Insurance product for the sake of obtaining a visa, or buying a policy because someone suggested it, is not the right way to approach the purchase of Travel Insurance. One must consider the following aspects of the insurance company before choosing a plan:

The purpose of any Travel Insurance policy is to ensure peace of mind to the traveller when they leave home for a holiday or on business. It is also required to cover any unforeseen expense that may come up due to medical or non medical reasons during the trip. One must realise and acknowledge that such exigencies are as likely to happen abroad as in India. This suggests that every traveller should protect themselves from financial loss even during their travels within India.

The most common excuses for not buying Travel Insurance for trips within India are:

Travel insurance is perhaps the best idea for an International Traveller. While current data suggests that travel insurance is the last thing on the travellers mind when they plan a trip to foreign shores, it is imperative that the discerning traveller gives way more importance to travel insurance than what is it currently being given. Experts would argue that having an insurance policy is as important as booking a hotel or a land tour package and that insurance should never be looked upon as an expense but as a mandatory investment. The purpose of insurance is to safeguard the financial status of the insured in the unfortunate and unforseen event of a claim – be it a medical expense or for any non medical cover like Baggage Loss or Delay, Trip Delay, Bounced Hotel, Missed Connection etc.

Ask a traveller who has lost his baggage or passport, or had a flight delayed and spent 12-18 hours at the airport, or someone who didn’t have a room to check into since the hotel had overbooked their customers, ask a traveller who has had to pay for his/her medical treatment through their personal savings and all of them will say that travel insurance should ideally be amongst the first few boxes to tick off when planning an International holiday.

Traveling across Europe is by and large covered by the introduction of the Schengen visa. If you are a traveler transiting through or visiting the Schengen countries, you have to obtain your Schengen visa from the Consulate of the country of your main destination. However, the proof of health insurance cover for your stay in the Schengen country has to be presented to the consulate prior to issuance of visa. The Schengen Visa requires that the insured traveler have an Accident & Sickness coverage of a minimum of Euros €30,000 covering the duration of the trip. The Schengen visa requirements also state that the insurance plan opted for by the insured needs to cover Emergency Medical Evacuation and Repatriation of Remains.

Hence some insurance companies offer a Schengen specific plan ensuring this minimum coverage is offered in their plans. The Schengen countries are Austria, Belgium, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Italy, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Norway, Poland, Portugal, Slovakia, Slovenia, Spain, Sweden and Switzerland. Hence if you are travelling to any of these countries, one must have a Schengen visa in place.

Yes, all travel insurance policies offer Emergency Accident & Sickness Medical Expenses coverage for both Inpatient and Outpatient treatment. The insurers offer multiple sum insured levels from $15,000 to $1,000,000 for Medical Expenses that the traveller can choose from. The medical expenses have a deductible which is the insured’s contribution to every claim. Please note that the benefit of Medical Evacuation and Repatriation of Mortal Remains is a subset of Medical Expenses as offered by the insurer

Some of the criteria include:

Yes, travel insurance can be bought immediately on completing the flight booking to ensure Trip Cancellation coverage is available from the date of purchase of the insurance policy. It should be noted that the travel insurance policy dates should ideally start one day before the flight date and upto a day after they are scheduled to return to India (For example if the travel is between 16th May and 21st June, then the insurance plan should ideally be between 15th May and 22nd June) to ensure coverage from the time the insured person leaves their home for the airport and returns home after their trip. Some insurance policies have Personal Accident coverage for this leg of the journey as well and that can be availed by the customer.

In any case, it is important that the traveller purchases their insurance policy prior to their departure from India.

Most insurance companies have a maximum entry age of 70 years on the date of commencement of travel for their Standard Plans. But almost all of them have a Senior Citizen Plan which is for travelers from 71 to 80/85 years of age and hence the traveler can avail this specific plan for their travel.

| Travel Insurers | Age Criteria |

|---|---|

| Apollo Munich Health Insurance | 6 months to 70 years |

| Bajaj Allianz General Insurance |

|

| Cholamandalam Travel Insurance |

|

| GO Digit General Insurance Limited |

|

| Future Generali India Insurance Co Ltd |

|

| HDFC Ergo General Insurance Co Ltd |

|

| Religare Health Insurance Company Limited |

|

| Reliance General Insurance Co Ltd |

|

| Royal Sundaram General Insurance Co Ltd |

|

| Tata AIG General Insurance Co Ltd |

|

No, as per the terms and conditions of the travel insurance policy, the travelling insured must be in India at the time of purchasing the policy. Hence the policy cannot be purchased post the commencement of the journey. However there are some insurance companies who will provide an exceptional approval post commencement of the journey subsequent to approvals from their underwriting team. This approval can if sought if there has not been too many days elapsed since the insured has travelled out of India and also after providing a good health and no claims declaration by the traveler. This approval process will be facilitated by the EIndia team…

Please ensure that you have received a soft copy of the insurance certificate post purchasing the same online. The policy certificate should be received by you along with the terms and conditions of the policy. Please go through the policy certificate to ensure that the coverage displayed is actually as per the coverage you had opted for. On every policy certificate, the Assistance Company (TPA) numbers abroad will be displayed. Most certificates will carry a Toll Free number as well as an email id for reaching out to the Assistance Company for any Claims or Travel related Assistance you may require. Please note that most of the numbers will require the traveler to have access to International Roaming so that you can call the Assistance company. Apart from the Assistance Company’s details, the certificate will also capture the Insurance company’s Customer Support details for the insured to reach out to incase they are unable to contact the Assistance Company. Some companies provide Country wise Toll free numbers that can be reached. In this case, please call the number marked against the country where you are currently based at to ensure you can reach them quickly. When you are attempting to contact the Assistance Company, please have your policy certificate details handy if in case the Assistance Partner needs to validate the policy status..

The deductible under the Accident & Sickness is normally USD $100 .The policy deductible is applicable for each instance of sickness/ailment. For continuous treatments relating to the same sickness, the deductible will only be applicable once. The insured is required to quote the Claim reference number when contacting the assistance company while undergoing follow up / re-revisit treatments. The deductible will need to be paid by the insured in each instance of a new/ different ailment / sickness. If the insured is claiming a reimbursement for incurred medical expenses, then the insurance company will reimburse the expenses less the deductible amount.

During discharge of the patient and on preparation of the final bill, the deductible mentioned in the policy schedule is payable by the insured. Apart from this, all expenses that are not payable under the terms and conditions of the policy will also have to be paid by the insured to the hospital / medical facilities. The Assistance/Insurance company will directly pay the allowed expenses to the hospital.

For example assuming that the deductible is $100, and if the medical expense incurred at $8500, then the insurance company will give a guarantee to the hospital to the extent of $8400 and instruct the hospital to collect the $100 directly from the insured at the time of discharge.

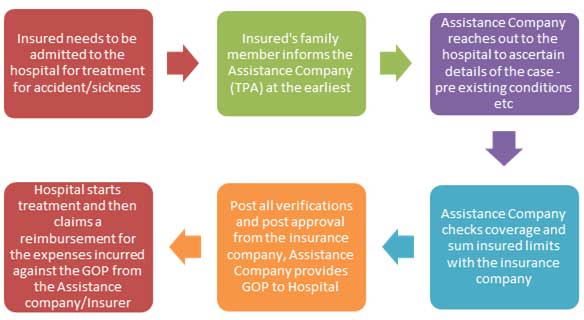

Yes, all travel insurance companies do offer direct/cashless settlement to hospitals for inpatient treatment for Accident of Sickness expenses incurred by the insured traveler. Direct settlement is more often referred to as cashless settlement or payment and is the process where the insurance company issues a Guarantee of Payment (GOP) letter to the medical institution (Hospital) confirming coverage for the insured against the treatment being availed by the insured. This GOP is issued to the hospital after the insurance company/its TPA confirms that the insured does have a valid policy and the treatment/ailment is actually covered under the scope of the policy terms and conditions.

It is important for the insured / family member of the insured to inform the Assistance company as soon as the insured is admitted to the hospital for treatment to ensure they don’t end up spending any money from their pocket except the deductible payable for every claim.

The process for Direct / Cashless Settlement is as follows:

There are two types of claims that an insured can file under a Travel Insurance policy. The first is a Cashless/Direct Settlement claim which is typically for Inpatient treatment for Accident & Sickness Medical expense claims.

The other type of claims are Reimbursement claims where the upfront expenses are incurred by the insured and then a reimbursement is sought from the Insurance company. Reimbursement claim are usually for Outpatient Medical Expense claims and for Non Medical claims like Passport Loss, Baggage Delay/Loss, Trip Delay, Missed Connection, Personal Accident etc. Here the insured is required to retain bills, receipts, documents pertaining to the expenses incurred and then submit the same to the insurance company on their return to India. The documents are submitted along with a claim form which narrates the type of loss incurred and other information including bank details, policy details etc. All insurance companies reimburse these claims against the documents submitted in a standard outer timeframe of 14 working days subject to policy terms and conditions.

The key factors include:

Holiday Insurance cost a fraction of the overall cost of the holiday when one takes into account the Airfare, Hotel Expenses and Tour Package Cost that the traveller would incur on their holiday. It is important that the traveller does not look at Travel Insurance as a cost but rather a necessity when one travels abroad given the cost of medical treatment in other countries and any unforeseen non medical exigency that can crop up like Passport Loss, Baggage Loss or Delay, Missed Connection or a Flight Delay.

Let’s look at a couple of examples; please note that insurance premiums will vary depending on Age of the insured, Destination and Duration of Travel and Coverage Sum Insured.

Situation A

According to the UNWTO 2018 Report, 51% of Global Travellers are on their way to Europe…Europe enjoys the distinction of being the continent of choice for the global traveller for many years now. Given the many breathtakingly beautiful destinations and the moderate climate throughout the year makes Europe an attractive destination for any traveller. However from an insurance perspective, Europe remains one of the costliest geographies for medical treatment. This is because of the strong Euro currency and continuously rising medical inflation.

Majority of Europe, which are 26 Schengen countries have a mandatory insurance policy for obtaining a visa and hence any traveller will need to first purchase an insurance policy. The Schengen visa requirements stipulate that the insurance coverage needs to be a minimum of Euros €30,000 for Accident & Sickness Expenses. It is important to note that all insurance companies should have an approval from the Schengen Committee for participating in the Schengen insurance program, only then can they underwrite a Schengen insurance program. Currently most of the leading travel insurers offer a specific plan for Schengen Travel which include Tata AIG, Bajaj Allianz, Religare, Reliance General, Royal Sundaram, Future Generali etc. As an insured, once can opt for any of them given their comprehensive coverage and competitive premium.

Currently 16% of the world travellers are visiting Americas (out of which majority of them are going to the USA) which is one of the largest market travel and tourism markets. A whopping 53% of the Indian outbound travellers are going to the The Americas and the largest % of them are going to USA. Most Indians travel there to visit family and friends and for their higher studies. USA is probably the costliest country for medical treatment and so while it is not mandatory for a traveller to have insurance before entering USA or for obtaining a visa, it is critical that the traveller does not take the risk of going to USA without insurance cover.

Given the way the medical system operates in the USA (with repricing of medical invoices) it is important that your travel insurance partner along with their Assistance and Claims Management partner (normally referred to as TPA) has a large network of hospitals across the country and also is aware of the medical landscape there. Most insurance companies have their TPA arrangements in USA but companies like Tata AIG have their Assistance arm Travel Guard based out of Houston which is a big value addition to the USA bound business, leisure or student traveller. The traveller should ensure sufficient coverage (atleast $100,000 sum insured for accident & sickness) and should ensure their plan has coverages like Personal Liability etc.

The deductible is a cost sharing requirement that the Insurer will not be liable to pay/indemnify/reimburse in case of travel insurance policies for Accident & Sickness and for a specified number of days/hours in case of hospital cash/non medical benefits which will apply before any benefits are payable by the Insurer. A deductible does not reduce the sum insured. The deductible is applicable per event.

For example, the deductible under Accident & Sickness is $100. This means for every medical claim, the insurance company will not settle the first $100 of the claim. So if the medical claim is $250, then the insured will get a reimbursement of $150 (Claim amount $250 – Deductible of $100). Similarly if the claim amount is $90, then the insured will not get any reimbursement since the claim amount is less than the deductible limit of $100.

Another example of a deductible is for a benefit like Trip/Flight Delay. The deductible in this case is 12 hours. This means that if the insured’s Trip/Flight is delayed due to Inclement Weather or Equipment Failure beyond 12 hours, then the insured will get a compensation from the insurance company as per the terms of the policy. However, if the flight is delayed for 8 hours, then there will be no compensation to the traveller since the delay is less than the deductible of 12 hours.

You are free to visit to any doctor/medical practitioner/hospital, provided they are licensed by the local Medical Council and acting within the scope of his/her/their license. The practitioner should hold a degree of a recognized institution and be registered by the Authorized Medical Council of the respective country. It is however advisable to call the Assistance Company (on their toll/toll free number) and seek their direction regarding the same.

Single Trip Insurance policies do not have a free look period. However an Annual Multi Trip period has a free look period of 15 days from the date of receipt of the Policy document to review the terms and conditions of this Policy provided no trip has been commenced. If the insured has any objections to any of the terms and conditions, the insured has the option of cancelling the Policy stating the reasons for cancellation and he/she will be refunded the premium paid for the policy, after adjusting the amounts spent on stamp duty charges and proportionate risk premium. The insured can cancel the policy only if the insured has not made any claims under the Policy.

The Insurance Company is committed to extend the best possible services to its customers. But there could be some situation wherein the insured may not be fully satisfied with the level of service or the decision made by an insurance company on a particular claim. If this is the case, then the insured, can lodge a complaint with the insurance company at their 24X7 Toll free number provided on the policy certificate, policy wordings (terms and conditions) or available on the company website. The insured can also choose to send an email to the customer service desk at the email id specified. After investigating the matter internally and subsequent closure, the insurance company will ideally send a response within a period of 10 days from the date of receipt of the complaint by the Company at its Head office or any of the branches. In case the resolution is likely to take longer time, the insurer will inform the insured of the same through an interim reply.

For lack of a response or if the resolution still does not meet the insured’s expectations, they can write to the Head - Customer Services at the insurance company. After examining the matter, they will send their final response within a period of 7 days from the date of receipt of your complaint. Within 30 days of lodging a complaint with the insurance company, if the insured still does not get a satisfactory response from the insurer, they can pursue other avenues for redressal of grievances, as well as directly approach Insurance Ombudsman appointed by IRDA under the Insurance Ombudsman Scheme.

The Insurance Ombudsman operates under Territorial jurisdiction

| Areas ofJurisdiction | Name of theOmbudsman | Contact Details |

|---|---|---|

| Gujarat, UT ofDadra & NagarHaveli, Damanand Diu | Shri P. Ramamoorthy | Insurance Ombudsman,

Office of the InsuranceOmbudsman,

2nd Floor, Ambica House,

Nr. C.U. Shah College,

Ashram Road,

AHMEDABAD-380 014

|

| Madhya Pradesh& Chhattisgarh | Insurance Ombudsman,

Office of the InsuranceOmbudsman,

JanakVihar Complex,

2 Floor, 6, Malviya Nagar,

Opp. Airtel, Near New Market,

BHOPAL(M.P.)-462 023

|

|

| Orissa | Shri B. P. Parija | Insurance Ombudsman,

Office of the InsuranceOmbudsman,

62, Forest Park,

BHUBANESHWAR-751 009

|

| Punjab,Haryana,HimachalPradesh, Jammu& Kashmir , UT of Chandigarh | Shri ManikSonawane | Insurance Ombudsman,

Office of the InsuranceOmbudsman,

S.C.O. No.101-103,

2nd Floor, Batra Building.

Sector 17-D,CHANDIGARH-160 017

|

| Tamil Nadu,UT– Pondicherry Town andKaraikal (whichare part of UTofPondicherry) | Insurance Ombudsman,

Office of the InsuranceOmbudsman,

Fathima Akhtar Court,

4th Floor, 453 (old 312),

Anna Salai, Teynampet,

CHENNAI-600 018

|

|

| Delhi & Rajasthan | Shri Surendra Pal Singh | Shri Surendra Pal Singh

Insurance Ombudsman,

Office of the InsuranceOmbudsman,

2/2 A, Universal Insurance Bldg.,

Asaf Ali Road,

NEW DELHI-110 002

|

| Assam,Meghalaya,Manipur,Mizoram,ArunachalPradesh,Nagaland andTripura | Shri D. C. Choudhury | Shri D.C. Choudhury,

Insurance Ombudsman

,

Office of the InsuranceOmbudsman,

“Jeevan Nivesh”, 5 Floor,

Near Panbazar Overbridge,

S.S. Road,

GUWAHATI-781 001 (ASSAM)

|

| Andhra Pradesh,Karnataka andUT of Yanam –a part of the UTof Pondicherry | Insurance Ombudsman

,

Office of the InsuranceOmbudsman,

6-2-46, 1 Floor, Moin Court,

A.C. Guards, Lakdi-Ka-Pool,

HYDERABAD-500 004

|

|

| Kerala , UT of (a)Lakshadweep,(b) Mahe – apart of UT ofPondicherry | Shri R. Jyothindranathan | Shri D.C. Choudhury,

Insurance Ombudsman

,

Office of the InsuranceOmbudsman,

2nd Floor, CC 27/2603,

PulinatBldg, Opp. Cochin Shipyard, M.G. Road,

ERNAKULAM-682 015

|

| West Bengal ,Bihar Jharkhand and, UT of Andaman& NicobarIslands | Ms. Manika Datta | Ms. Manika Datta

Insurance Ombudsman,

,

Office of the InsuranceOmbudsman,

4th Floor, Hindusthan Bldg.

Sikkim Annexe, 4, C.R.Avenue,

Kolkatta – 700 072

|

| Uttar Pradeshand Uttaranchal | Shri G. B. Pande | Insurance Ombudsman,

,

Office of the InsuranceOmbudsman,

Jeevan Bhawan, Phase-2,

6th Floor, Nawal Kishore Road,

Hazaratganj,

LUCKNOW-226 001

|

| Maharashtra ,Goa | Insurance Ombudsman

,

Office of the InsuranceOmbudsman,

S.V. Road, Santacruz(W),

MUMBAI-400 054

|

No. Any complainant, whose complaint on the same subject matter is or was before a Court/Consumer Forum or an Arbitrator cannot approach an Insurance Ombudsman.

The Ombudsman will receive and consider complaints or disputes relating to:

Yes. No complaint to the Insurance Ombudsman shall lie unless the complaint is made within one year:

Yes, IRDA has implemented the Integrated Grievance Management System (IGMS). IGMS provides a gateway for policyholders to register complaints with insurance companies first and if need be escalate them to the IRDA Grievance Cells. It uses Web interface to ensure that it is accessible at all places and is on real time. It has also a mechanism to capture complaints received in physical as well as email form or voice calls received by IRDA Grievance Call centre (IGCC).

Also IRDA Grievance Call Centre (IGCC) can be accessed through

Some of the typical exclusions under the Travel policy will include:

The Assistance Company is the partner abroad who is available to assist the insured during any medical or non medical emergency. They are normally referred to as the Third Party Administrator (TPA). Most insureds assume that the Assistance Company is only there for support during medical emergencies, but they do also support in many non medical situations as well. They normally provide the following services:

A ‘Pre-Existing Illness/Condition’ is one with which the person is already suffering from and is availing ongoing medical treatment when he/she buys the policy. It could also be related to a major surgery that the insured has had in the recent past. Some insurance plans do not cover pre-existing diseases, whereas a few others cover the condition in “Life Threatening situations”.

A pre existing condition means any condition, ailment or injury or related condition(s) for which the insured had signs or symptoms, and / or were diagnosed, and / or received medical advice/ treatment, within 48 months prior to commencement of the first Policy issued by the Insurer. This means that if the insured is traveling abroad with a pre existing condition and avails of any treatment abroad, the insurance company will not be liable for paying the claim.

The insurance company normally goes by the guidance of the attending physician in the medical facility abroad while deciding whether a condition is pre existing or not. If the attending physician declares that the cause of the treatment is a pre existing condition carried by the insured, then the treatment costs will not be reimbursed under the policy.

Some insurance companies offer a limited coverage for medical expenses arising due to pre existing conditions, when the situation is Life threatening in nature.

A Life threatening condition is an unforeseen medical emergency, which puts the life of the insured at extreme risk. In such event, measures solely designed to relieve acute pain, provided to the Insured by the Physician for Disease/accident arising out of a pre-existing condition would be reimbursed upto a limit specified in the policy terms and conditions. The treatment for these emergency measures would be paid till the insured becomes medically stable or is relieved from acute pain. All further medical cost to improve or maintain medically stable state or to prevent the onset of acute pain would have borne by the Insured.

It is important to be noted that all plans displayed on the eIndiaInsurance website do not offer coverage for pre existing conditions. Hence the traveller should review the plan prior to purchasing the same, if they are looking for such a cover. If the traveller still has clarifications regarding the same, it is better to speak to our customer service executive.

A pre-existing condition usually means any medical condition for which medical advice, diagnosis, care or treatment was recommended or received. It is always a good idea to speak to the insurer you are thinking of using to check whether they will include your condition on the policy. For example, If you're pregnant, certain exclusions may apply if you travel after a certain point during the period of your pregnancy. We would advise you to read the policy wording thoroughly, prior to purchasing the plan to see at what exclusions and other conditions may be in place.

Medical costs abroad can be very expensive and without adequate insurance cover you could be left severely out of pocket.

While the policy certificate of most insurance companies may not explicitly state the availability of coverage for pre-existing diseases on the face of the policy certificate, the policy terms and conditions which are shared with your along with the certificate, will state that this coverage is available, subject to prescribed limits, terms and conditions.

A pre existing condition means any condition, ailment or injury or related condition(s) for which the insured had signs or symptoms, which was diagnosed and for which the insured received medical advice/ treatment, within 48 months prior to commencement of the first Policy issued by the Insurer. This means that if the insured is traveling abroad with a pre existing condition and avails of any treatment abroad, the insurance company will not be liable for paying the claim.

The insurance company normally goes by the guidance of the attending physician in the medical facility abroad while deciding whether a condition is pre existing or not. If the attending physician declares that the cause of the treatment is a pre existing condition carried by the insured, then the treatment costs will not be reimbursed under the policy.

Some insurance companies offer a limited coverage for medical expenses arising due to pre existing conditions, when the situation is Life threatening in nature

If you have had the knee replacement surgery within 48 months prior to commencement of your travel/trip, then the same will be treated as a pre existing condition under the policy and any claim/treatment occurring as a result of the surgery, will not be covered under the policy. Some insurance policies have a limited coverage for pre-existing conditions in life threatening conditions, this could provide some coverage subject to other terms and conditions of the policy.

If you have had the bypass surgery within 48 months prior to commencement of your travel/trip, then the same will be treated as a pre-existing condition under the policy and any claim/treatment occurring as a result of the surgery, will not be covered under the policy. Similarly if 48 months have elapsed since the surgery, but you are still under continuous medication for the bypass, the same will be treated as a pre-existing condition and excluded under the policy. Some insurance policies have a limited coverage for pre-existing conditions in life threatening conditions, this could provide some coverage subject to other terms and conditions of the policy.

If you are still under continuous medication for diabetes, the same will be treated as a pre-existing condition and excluded under the policy. Some insurance policies have a limited coverage for pre-existing conditions in life threatening conditions, this could provide some coverage subject to other terms and conditions of the policy, if the life threatening condition is a result of you being a diabetic.

Yes. No complaint to the Insurance Ombudsman shall lie unless the complaint is made within one year:

For any Indian traveller who is going abroad, it is very important to purchase travel insurance. While it is not a mandatory product for travel to most countries abroad (except Schengen, UAE and Australia (for certain age groups)), having an insurance cover can give the traveller peace of mind in case of any unforeseen exigency (medical or non-medical) while they are enjoying their holiday/business trip. As most travellers will be aware, the cost of any medical treatment is astronomical when compared to India and hence the traveller could end up spending a large part of their savings for treatment abroad in case of an unfortunate accident or sickness. The cost of insurance is a fraction of the most of medical treatment and hence it is advisable to travel abroad with insurance. Secondly there are many non medical emergencies like Loss of Passport, Baggage Loss / Delay, Flight Delay, Trip Cancellation, Missed Connection etc that can be covered and this will not result in a financial loss to the traveller.

It may be surprising to note that insurance is not as costly a product as it is perceived to be. (For example for a 35 year old traveller to Asia for a period of 5 days, the insurance premium across 10 products from 5 insurance companies ranges from ₹334 to ₹491 for the whole trip – this is cost of a cup of coffee/burger at the International Airport. And this is for an average coverage of USD $25,000 which is around ₹17,00,000 for Accident & Sickness). While longer duration travel to more developed nations like USA, Europe, UK will have higher premiums, these premiums are related to the cost of medical treatment in those respective countries and they can be very costly for an Indian traveller given the relative weakness of the Indian Rupee ₹. Even for Students going abroad for their studies, the Indian insurers do offer competitively priced insurance plans with comprehensive benefits at a much cheaper premium than what the student will end up shelling out at the University for a similar coverage. Hence it is strongly recommended that every traveller buys an insurance policy before leaving India.

It is not fair to state that any insurance plan is better or worse than another plan. What is important to note that each insurance plan comes with a different set of benefits at varying sum insureds and it is important for the insured to compare the options available before making a decision. There are two aspects to travel insurance. One is the set of benefits/coverages under the plan. Hence the insured must consider the following while deciding on the insurance plan and company – Duration of Travel, Destination of Travel, Age of the Traveller, Coverage required. A younger traveller can opt for a lesser coverage while an older traveller should take a more comprehensive cover with higher benefits . Second and more importantly the insured should consider the Assistance and Claims support available in the foreign location. It is better to partner with an insurance company who has a strong Assistance partner and a large network of hospitals abroad. This will ensure seamless cashless treatment and prompt travel and claims assistance should the need arise.

The traveller must consider the following while deciding on the insurance plan and company – Duration of Travel, Destination of Travel, Age of the Traveller, Coverage required. EIndia actually does this comparison work for the traveller. Once this information is provided, EIndia will collate all the information and present in a tabular form the insurance plans/premiums offering the required coverages and this process makes it easier for the traveller to make an informed decision. Once should not assume that the cheapest insurance premium policy has the least coverages or vice versa. The traveller should have the comparison and then decide based on the coverage and premium and reputation of the insurance company. There are many strong travel insurance providers who have been offering travel insurance solutions for many years and have been settling claims promptly and these providers should be evaluated before finally choosing your insurance partner.

Cheapest insurance often represents the insurance plan which offers the least premium to the traveller. These plans normally come with lesser sum insureds and coverages for the traveller and hence it is prudent for the traveller to not only look at the premium but also compare the benefits of the plans available before making an informed choice. Given that the traveller is already spending reasonably large monies for their tickets and hotels, there is a tendency to cut corners on the insurance policy and buy the one with the least premium. By spending a little more effort and a slightly higher premium outlay, the traveller could end up buying a relatively more comprehensive insurance plan that just the cheapest insurance policy which if the best way to proceed. A cheaper premium plan could also mean that the deductible (insured’s contribution to a claim) is higher which may result in the insured shelling out a higher part of the claim incurred later during the trip. Hence it is advisable that the traveller compares like products (apples with apples) before arriving at the optimum plan.

Ideally the traveller must buy travel insurance once they have finalise their travel plans and booked their air tickets and hotels/tour packages. The specific reason for booking the insurance at this stage is that for any unforeseen yet covered reasons if the traveller’s trip is cancelled and they have a Trip Cancellation benefit in their insurance plan, then they can make a claim for the non refundable part of the Air Tickets/Hotel & Tour Bookings even before their trip would’ve started. Covered cancellation reasons include:

Single Trip Insurance policies do not have a free look period. However an Annual Multi Trip period has a free look period of 15 days from the date of receipt of the Policy document to review the terms and conditions of this Policy provided no trip has been commenced. If the insured has any objections to any of the terms and conditions, the insured has the option of cancelling the Policy stating the reasons for cancellation and he/she will be refunded the premium paid for the policy, after adjusting the amounts spent on stamp duty charges and proportionate risk premium. The insured can cancel the policy only if the insured has not made any claims under the Policy.

It is important for all travellers to note that the Travel Insurance policies are not just coverage for Medical Expenses, both Accident and Sickness…there are many important non medical covearges, most of which are listed below:

Tips to find good and adequate international travel health insurance.

Know more »Comparison of overseas Healthcare cost and popular tourist destinations.

Know more »How to use visitor insurance in case of sudden sickness and accidents.

Know more »Visa free countries for Indians - Check, list of visa free countries where Indian passport holders can travel without visa.

Know more »Indian passport holders have the benefit of visa on arrival in different countries – find travel insurance suitable for visa on arrival.

Know more »You can buy insurance online by using a credit/debit card, UPI, direct funds transfer using NEFT or RTGS or by using a cheque.

Know more »Travelers who have already traveled from India and do not have insurance can buy travel medical insurance after approval.

Know more »Insurance customers can renew their existing policy online before the exipry date at any time.

Know more »In case of a claim or reimbursement of treatment expenses, notify by contacting them.

Know more »Tips on Air Travel – Safety, Comfort and Wellness. Air travel tips for first time.

Know more »Are travel insurance directly billed or is it reimbursement basis, is there a hospital network.

Know more »How to use Indian visitor insurance in case of sudden sickness and accidents

Know more »Comparison of healthcare cost in Indian and other popular Indian tourist destinations

Know more »Tips to find good and adequate international travel insurance from finest insurance companies in India

Know more »